- Analysis finds the updated “Better Care Reconciliation Act” (BCRA) could cause collapse of individual markets within three to five years (especially if the Consumer Freedom Option is included).

- Health insurance under the BCRA would cost consumers much more and cover far less.

- Stabilization funding included in the bill would need to be five times higher than proposed to offset new policies that would make markets less stable.

- Federal policy makers can improve markets and save money in the short term by providing risk stabilization support through reinsurance, which helps keep premiums affordable for all.

- Individual market stabilization would be fostered by assuring the ongoing provision of direct federal funding of cost-sharing reduction payments for consumers through 2017 and 2018.

“Activities in Washington are moving quickly, but the reality on the ground is moving even faster,” said Peter V. Lee, executive director of Covered California. “The need to stabilize the markets in 2018 requires immediate action — before the summer recess.”

The reports issued highlight important issues for federal policymakers affecting the individual market for health coverage:

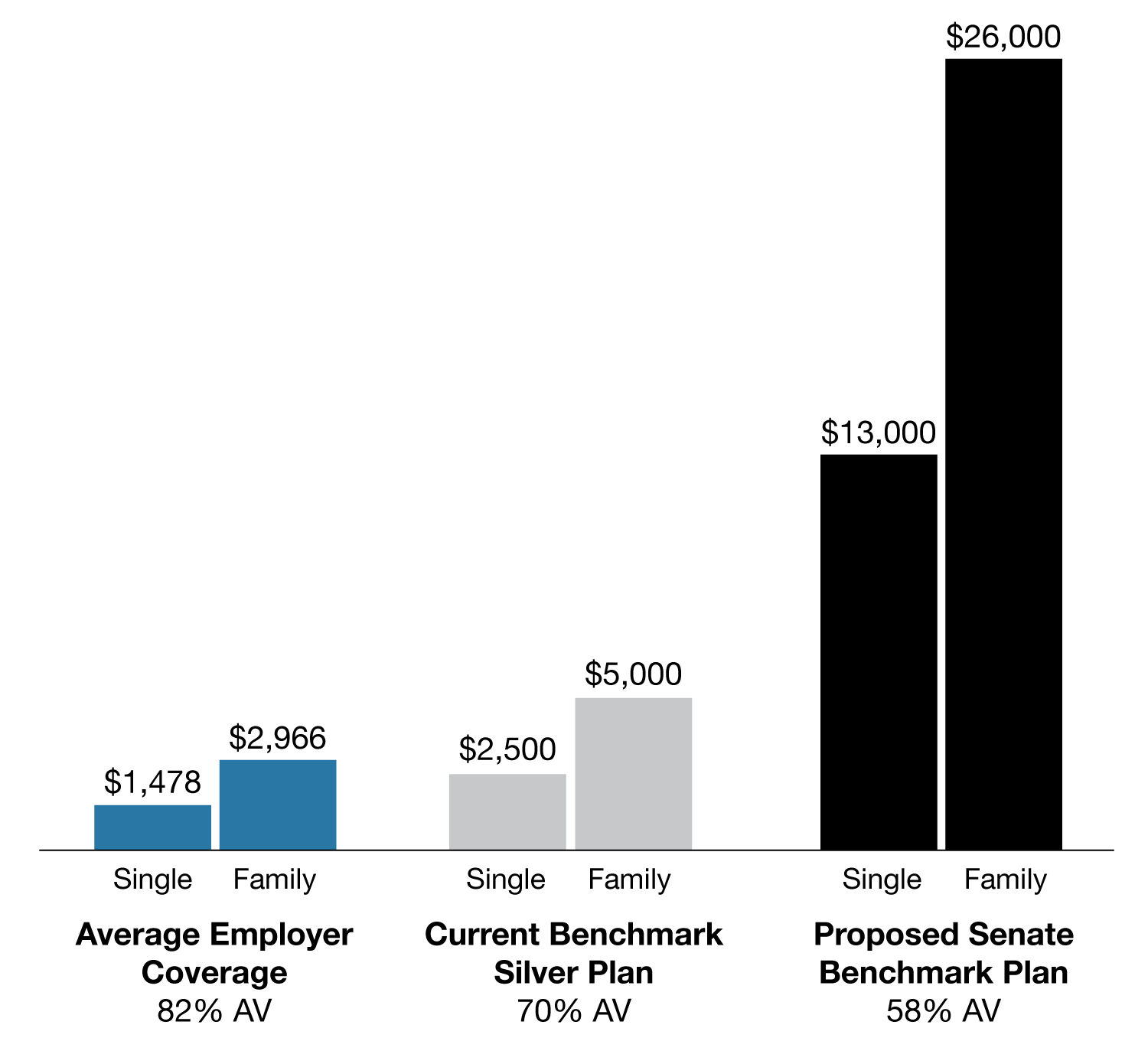

· The quality and value of coverage. Covered California’s analysis released Friday shows the Better Care Reconciliation Act (BCRA) includes changes that would increase the price of care and diminish the quality of health coverage available to Americans who buy coverage in the individual market. In particular, the new “benchmark” plan would mean that for those getting subsidies, the deductible would increase to $13,000 for an individual and $26,000 for a family. (See, “Stability Lost – Implications for Consumers and the Individual Insurance Market Under the Senate Proposal”).

· Adequacy of stabilization funding. While “risk stabilization” funding mechanisms can be effective, the resources proposed in the BCRA are insufficient. Stabilization funding would need to be increased by many times over the levels proposed in the BCRA for 2022 and beyond to offset the destabilizing effects of other policy elements in the bill. (See, “Stability Lost – Implications for Consumers and the Individual Insurance Market Under the Senate Proposal”).

· Ongoing funding of cost-sharing reduction payments. The mechanics and value of the cost-sharing reduction payments are outlined in the paper, “How Cost-Sharing Reductions Work and the Critical Role They Play in the Individual Market,” which describes how these payments lower costs for millions of Americans who receive them, lower costs for everyone in the individual market by improving the risk mix, and help the federal government save money.

· The value of using reinsurance as a risk stabilization tool. The report, “Funding Reinsurance to Support Risk Stabilization and Potentially Reduce Federal Spending on Advanced Premium Tax Credits,” shows how reinsurance lowers premiums for everyone in the individual market, as well as the financial mechanics that underlie the fact that a $20 billion reinsurance fund that could lower premiums for everyone in the individual market by 12 percent to 18 percent and would cost the federal government less than $7 billion since the cost of premium tax credits borne by the government would be greatly reduced.

Reinsurance and funding for cost-sharing reductions are short-term, immediate changes that could improve health care markets in 2018 for Americans needing affordable coverage. Covered California’s Chief Actuary noted the efficacy of reinsurance programs: “Reinsurance programs could be administered virtually overnight and the payoff for consumers could be to immediately reduce premiums for 2018,” said John Bertko. He added, “One of the nice financial benefits is that a reinsurance program of $20 billion would only cost the government about $7 billion because of the reduced federal subsidy payments — that’s good math.”Cost-sharing reduction payments also ensure the individual market works for all consumers. “Far from being a ‘bailout,’ cost-sharing reductions ensure that health coverage has value for low-income consumers,” Lee said. “The federal government making clear its ongoing commitment to make these payments is vital to the stability of the individual markets across the nation.”

Among the highlights in the reports, Covered California reports on how the quality of health care coverage would dramatically diminish under the BCRA because the bill proposes a new, lower “benchmark plan” with a 58 percent actuarial value (AV). Consumers would bear additional costs in the form of significantly higher deductibles compared to employer-based coverage and the current 70 percent AV Silver benchmark plan available on the individual market today (See Figure 1: Benchmarking Consumer Impact of Plan Design Deductibles)

Figure 1: Benchmarking Consumer Impact of Plan Design Deductibles

Table 1 shows how two current forms of health coverage compare with the proposed benchmark coverage in the BCRA:

Table 1: Benchmarking Consumer Impact of Plan Designs

In addition, the reports point out other challenging elements of the BCRA. Table 2 looks at how the proposed stabilization funding in the BCRA would affect a variety of scenarios. In each case, stabilization funding offered in the BCRA is a fraction of what would be necessary to account for the upheaval caused by the bill and results in a multi-billion dollar shortfall during every year between 2022 and 2026.

“The stabilization funding appears to be inadequate and many times the current level would be needed to protect consumers,” Lee said.

Table 2: Modeling Impacts of BCRA State-Administered Stabilization Funds

The reports also highlight the value of two provisions that could have immediate positive effects for 2018 in keeping premiums down and help consumers access the coverage they need. “A risk stabilization fund of $20 billion, paid as reinsurance, helps lower premiums by up to 18 percent which helps make coverage more affordable,” Lee said, “while cost-sharing reductions help consumers who are covered get the care they need by lowering their out-of-pocket expenses.”

The reports show that both programs not only promote a healthier risk pool and lower premiums, but they provide good value for the federal government.

Finally, the report examines the Consumer Freedom Option amendment offered by U.S. Senator Ted Cruz that would allow health insurance companies to offer cheaper plans with much fewer benefits off exchange as long as they also offer a plan that complies an Affordable Care Act compliant plan on exchange. The analysis found this would significantly destabilize and possibly collapse the individual market by splitting the risk pool, with healthy consumers transitioning to off-exchange coverage, leaving sicker consumers enrolled in exchanges.

“Allowing bare bone plans destroys the risk pool,” said Bertko. “The Consumer Freedom Option would have a devastating effect on the market.”

Lee said the changes being considered come at a time when many states are actually seeing their individual markets stabilize. He said a recent study by the Centers for Medicare and Medicaid Services shows risk scores stabilizing across the nation, while an analysis by the Kaiser Family Foundation found that health plans’ first-quarter 2017 profit margins have reached breakeven or modest profit levels.

“While there are improvements that can be made, the individual market is functioning better in many places than it was before the Affordable Care Act was enacted,” Lee said. “Rather than improving the market, the changes being considered in the U.S. Senate would put it in grave danger and threaten access to health coverage and care for millions of people.”

About Covered California

Covered California is the state’s health insurance marketplace, where Californians can find affordable, high-quality insurance from top insurance companies. Covered California is the only place where individuals who qualify can get financial assistance on a sliding scale to reduce premium costs. Consumers can then compare health insurance plans and choose the plan that works best for their health needs and budget. Depending on their income, some consumers may qualify for the low-cost or no-cost Medi-Cal program.

Covered California is an independent part of the state government whose job is to make the health insurance marketplace work for California’s consumers. It is overseen by a five-member board appointed by the governor and the Legislature. For more information about Covered California, please visit www.CoveredCA.com.